Audit Services

GST Audit

Audit under GST involves examination of records, returns and other documents maintained by a GST registered person. It also ensures correctness of turnover declared, taxes paid, refund claimed, input tax credit availed and assess other such compliances under GST Act to be checked by an authorized expert.

GST is a trust-based taxation regime wherein a taxpayer is required to self-assess his tax liability, pay taxes and file returns. Thus, to ensure whether the taxpayer has correctly self -assessed his tax liability a robust audit mechanism is a must. Various measures are taken by the government for proper implementation of GST and audit is one amongst them.

Internal Audit

Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization's operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control and governance processes.

Internal auditing is a catalyst for improving an organization's governance, risk management and management controls by providing insight and recommendations based on analyses and assessments of data and business processes. With commitment to integrity and accountability, internal auditing provides value to governing bodies and senior management as an objective source of independent advice. Professionals called internal auditors are employed by organizations to perform the internal auditing activity.

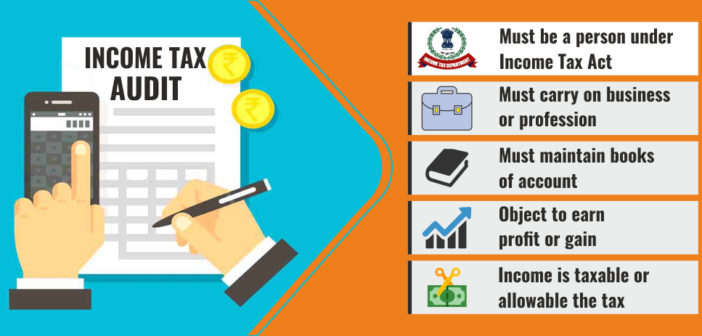

Income Tax Audit

The Income Tax audit is an examination of an individual's or organisation's tax returns by any outside agency to verify that all the income, expenditure and deduction information are filed correctly.

The dictionary meaning of the term "audit" is check, review, inspection, etc. There are various types of audits prescribed under different laws like company law requires a company audit, cost accounting law requires a cost audit, etc. The Income-tax Law requires the taxpayer to get the audit of the accounts of his business/profession from the view point of Income-tax Law.